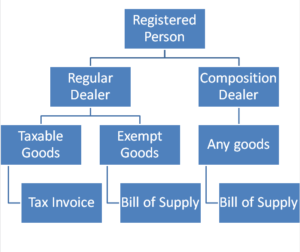

Composition Scheme under GST

Concept of Composition Scheme is commonly known to every person because it was also available in Central Excise Duty laws and in State VAT law too. Composition scheme is an opportunity provided to small traders, manufacturers and restaurant…

Recent Comments