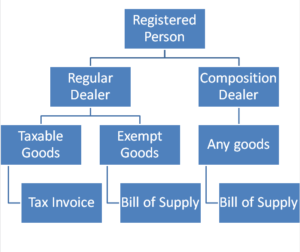

Types of Invoices in GST

There are various types of invoice (s) to be issued under GST at different situations :

| Situation | Type of Invoice |

| Registered person supplying taxable goods/services/both | Tax Invoice |

| Registered person supplying exempted goods/services/both | Bill of Supply |

| Registered person supplying taxable as well as exempted goods/services/both | Invoice-cum-Bill of Supply |

| Composition Dealer | Bill of Supply |

| Receipt of Advance Payment | Receipt Voucher |

| Refund of advance payment | Refund Voucher |

| Purchase from Un-registered dealer (liable to tax under RCM) | Purchase Invoice |

| Payment against purchases from Un-registered dealer (liable to tax under RCM) | Payment Voucher |

| Rectification in Invoice | Credit Note or Debit Note |

Tax Invoice

Tax invoice is required to be issued for all taxable goods or services or both supplied by a registered person to any person. Tax Invoice under GST must reflect following components:

|

Tax Invoice to registered person |

Tax Invoice to unregistered person |

|

|

Additional requirement in case of Export:

- The invoice shall carry an endorsement :

“SUPPLY MEANT FOR EXPORT ON PAYMENT OF INTEGRATED TAX” or

“SUPPLY MEANT FOR EXPORT UNDER BOND OR LETTER OF UNDERTAKING WITHOUT PAYMENT OF INTEGRATED TAX”,

- Name and address of recipient

- Address of delivery

- Name of Country of Destination

HSN Code requirement

|

Turnover in preceding Financial Year |

HSN Code required |

|

Upto Rs 1 Crore 50 Lakh |

Not require |

|

More than Rs 1.50 Crore and upto Rs 5 Crore |

Upto 2 digits |

| More than Rs 5 Crore |

Upto 4 digits |

Manner of issuing Tax Invoice

In case of supply of Goods

The invoice shall be prepared in triplicate, in case of supply of goods, in the following manner:-

(a) the original copy being marked as ORIGINAL FOR RECIPIENT;

(b) the duplicate copy being marked as DUPLICATE FOR TRANSPORTER.

(c) the triplicate copy being marked as TRIPLICATE FOR SUPPLIER.

In case of supply of Services

The invoice shall be prepared in duplicate, in case of supply of services, in the following manner:-

(a) the original copy being marked as ORIGINAL FOR RECIPIENT; and

(b) the duplicate copy being marked as DUPLICATE FOR SUPPLIER.

Time Limit to issue Tax Invoice

| In case of Sale of Goods | In case of Sale of Services |

| One time Supply

Before or at the time of : (a) Removal of goods where movement of goods (b) Delivery of goods or making available thereof |

One Time Supply

Before provision of services; or Within 30 days after provision of services

|

| Continuous Supply

Before or at the time of :

|

Continuous Supply

|

| Cessation of Supply of services before completion

Invoice shall be issued at the time of cessation for the value shall be determined to the extent of supply made before such cessation. |

|

Goods sent on approval basis:

|

|

Any situation where Invoice Not required on sale ?

Registered person may not issue a tax invoice/bill of supply if the value of the goods or services or both supplied is less than two hundred rupees.

Tax invoice of such value may not be issued, if:

- the recipient is not a registered person; and

- the recipient does not require such invoice.

In this case, a consolidated tax invoice shall be issued at the close of each day in respect of all sales.

Bill of Supply

Bill of supply is required to be issued for all exempted goods or services or both supplied by a registered person to any person.

If a dealer is registered under Composition Scheme of GST, he is obliged to issue a Bill of Supply instead of Tax Invoice.

Bill of Supply under GST must reflect following components:

- name, address and Goods and Services Tax Identification Number of the supplier;

- a consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters – hyphen or dash and slash symbolized as “-” and “/” respectively, and any combination thereof, unique for a financial year;

- date of its issue;

- name, address and Goods and Services Tax Identification Number or Unique Identity Number, if registered, of the recipient;

- Harmonized System of Nomenclature Code for goods or services;

- description of goods or services or both;

- value of supply of goods or services or both taking into account discount or abatement, if any; and

- signature or digital signature of the supplier or his authorized representative.

Please note : Any tax invoice or any other similar document issued under any other Act for the time being in force in respect of any non-taxable supply shall be treated as a bill of supply for the purposes of the Act.

Note for Composition Dealer : At the top of every invoice, composition dealer must write the following statement :

“Composition Taxable Person, Not Eligible to collect TAX on supplies”

Additional requirement in case of Export

- The invoice shall carry an endorsement :

“SUPPLY MEANT FOR EXPORT ON PAYMENT OF INTEGRATED TAX” or

“SUPPLY MEANT FOR EXPORT UNDER BOND OR LETTER OF UNDERTAKING WITHOUT PAYMENT OF INTEGRATED TAX”,

- Name and address of recipient

- Address of delivery

- Name of Country of Destination

HSN Code requirement

|

Turnover |

HSN Code required |

|

Upto Rs 1 Crore 50 Lakh |

Not require |

|

More than Rs 1.50 Crore and upto Rs 5 Crore |

Upto 2 digits |

| More than Rs 5 Crore |

Upto 4 digits |

Concept of Invoice-cum-Bill of Supply

A new concept of ‘Invoice-cum-Bill of Supply’ has been inserted under Invoice rules of GST through N/N 45/2017 dtd 13.10.2017

Till 13.10.2017, every registered person supplying taxable as well as exempted goods/services/both had to issue ‘Tax Invoice’ for taxable supplies and ‘Bill of Supply’ for exempted supplies. After the above said concept being incorporated in GST law, such registered person could issue single invoice for both type of supplies in single document. Such composite document will be called as “Invoice-cum-Bill of Supply”.

However, Invoice-cum-Bill of Supply can be issued only for supplies to unregistered persons.

In case of supply to registered persons, Tax invoice and Bill of Supply needs to be separately issued for respective supplies.

Receipt Voucher

In case of advance receipt from any customer, a receipt voucher to be issued. It should reflect following components:

(a) name, address and Goods and Services Tax Identification Number of the supplier;

(b) a consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters hyphen or dash and slash symbolised as “-” and “/” respectively, and any combination thereof, unique for a financial year;

(c) date of its issue;

(d) name, address and Goods and Services Tax Identification Number or Unique Identity Number, if registered, of the recipient;

(e) description of goods or services;

(f) amount of advance taken;

(g) rate of tax (central tax, State tax, integrated tax, Union territory tax or cess);

(h) amount of tax charged in respect of taxable goods or services (central tax, State tax, integrated tax, Union territory tax or cess);

(i) place of supply along with the name of State and its code, in case of a supply in the course of inter-State trade or commerce;

(j) whether the tax is payable on reverse charge basis; and

(k) signature or digital signature of the supplier or his authorised representative:

Where at the time of receipt of advance :-

the rate of tax is not determinable, the tax shall be paid at the rate of eighteen per cent.;

the nature of supply is not determinable, the same shall be treated as inter-State supply.

Refund Voucher

Refund voucher is issued at the time of refund of advance amount received earlier. A refund voucher should contain followings contents:

(a) name, address and Goods and Services Tax Identification Number of the supplier;

(b) a consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters hyphen or dash and slash symbolised as “-” and “/” respectively, and any combination thereof, unique for a financial year;

(c) date of its issue;

(d) name, address and Goods and Services Tax Identification Number or Unique Identity Number, if registered, of the recipient;

(e) number and date of receipt voucher issued in accordance with the provisions of rule 50;

(f) description of goods or services in respect of which refund is made;

(g) amount of refund made;

(h) rate of tax (central tax, State tax, integrated tax, Union territory tax or cess);

(i) amount of tax paid in respect of such goods or services (central tax, State tax, integrated tax, Union territory tax or cess);

(j) whether the tax is payable on reverse charge basis; and

(k) signature or digital signature of the supplier or his authorised representative.

Purchase Invoice

Purchase Invoice to be issued in case of purchases of taxable goods and services from un-registered dealers for which tax is liable to pay under reverse charge.

Please note in case of goods or services purchased from registered dealers and that goods or services are liable to tax under reverse charge, then, Purchase invoice is not required to be issued. This is because registered person is already under obligation to issue tax invoice even if goods or services are liable to tax under reverse charge mechanism.

Invoice requirement – where goods or services are specified to be taxed under Reverse Charge and provider of such supplies is unregistered person

In this case, a registered person will issue invoice for each supplies of any value on independent basis.

Invoice requirement – where taxable goods or services (Other than specified) purchased from unregistered dealer liable to be charged to tax under Reverse Charge

In this case, a registered person may issue a consolidated invoice at the end of a month for supplies, where the aggregate value of such supplies exceeds rupees five thousand in a day from any or all the suppliers.

Contents of Purchase Invoice: All contents as required in Tax Invoice should be available in Purchase Invoice

Credit Notes and Debit Notes

Credit Notes and Debit Notes are required to be issued only against Tax Invoice. These are not required to be issued against Bill of Supply. Following are some provisions in relation to Credit and Debit Notes.

|

Credit Notes |

Debit Note / Supplementary Invoice |

Circumstances/Reason to issue

|

Circumstances/Reason to issue

|

| Maximum Time Limit to issue a Credit Note

Credit note in respect of an invoice should be issued earlier of :

|

There is no Time Limit to issue a Debit Note

|

| Effect of Credit Note: Decrease in Tax Liability | Effect of Debit Note: Increase in Tax Liability |

Relevancy of Time limit to issue a Credit Note:

Credit Note impacts GST Output liability. Dealer can claim reduction in output liability in the return of month in which such credit note issued.

If Credit note issued after expiry of above said time limits, dealer can’t claim reduction in output tax liability.

One more restriction against reduction in output tax liability (due to Credit Note) is that if the incidence of tax and interest on such supply has not been passed on to any other person, such reduction can’t be claimed.

Contents of Credit Note/ Debit Note

- name, address and Goods and Services Tax Identification Number of the supplier;

- nature of the document;

- a consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters hyphen or dash and slash symbolised as “-” and “/” respectively, and any combination thereof, unique for a financial year;

- date of issue of the document;

- name, address and Goods and Services Tax Identification Number or Unique Identity Number, if registered, of the recipient;

- name and address of the recipient and the address of delivery, along with the name of State and its code, if such recipient is un-registered;

- serial number and date of the corresponding tax invoice or, as the case may be, bill of supply;

- value of taxable supply of goods or services, rate of tax and the amount of the tax credited or, as the case may be, debited to the recipient; and

- signature or digital signature of the supplier or his authorised representative.

Concept of Revised Invoice

Every registered person, who has been granted registration with effect from a date earlier than the date of issuance of certificate of registration to him, may issue revised tax invoices in respect of taxable supplies made during the period starting from the effective date of registration till the date of the issuance of the certificate of registration.

However, in case of taxable supplies made to unregistered persons within same state, registered person may issue a consolidated revised tax invoice in respect of all taxable supplies to unregistered persons during such period.

Further, in the case of inter-State supplies to un-registered persons, where the value of a supply does not exceed two lakh and fifty thousand rupees, a consolidated revised invoice may be issued separately in respect of all the recipients located in a State.

Contents of Revised Invoice

- The word “Revised Invoice”, wherever applicable, indicated prominently

- name, address and Goods and Services Tax Identification Number of the supplier;

- nature of the document;

- a consecutive serial number not exceeding sixteen characters, in one or multiple series, containing alphabets or numerals or special characters hyphen or dash and slash symbolised as “-” and “/” respectively, and any combination thereof, unique for a financial year;

- date of issue of the document;

- name, address and Goods and Services Tax Identification Number or Unique Identity Number, if registered, of the recipient;

- name and address of the recipient and the address of delivery, along with the name of State and its code, if such recipient is un-registered;

- serial number and date of the corresponding tax invoice or, as the case may be, bill of supply;

- value of taxable supply of goods or services, rate of tax and the amount of the tax credited or, as the case may be, debited to the recipient; and

- signature or digital signature of the supplier or his authorised representative.

Invoicing relaxation for newly registered dealers:

A Registered person within 30 days from issuing of Registration Certificate, issue a revised invoice for Invoices issued from the effective date of registration and date of Registration Certification

For additional requirements for transport sector, please refer our other article:

GST for Transporters providing goods transport services by road (GTA Services)