After more than two years, government now succeeds to provide fully online module for application, processing, issuance and disbursement of eligible refunds under GST Laws. As per Circular no. CIR-125/44/2019-GST dated 18/11/2019, government has clarified that it is fully ready for online processing of refunds w.e.f. 26/09/2019.

This circular is being issued as a Master Circular superseding all the earlier circulars for clarifying procedure of issuance of GST refunds. As per this, online module for following category of refunds are fully operational w.e.f. 26/09/2019 :-

a. Refund of unutilized input tax credit (ITC) on account of exports without payment of tax;

b. Refund of tax paid on export of services with payment of tax;

c. Refund of unutilized ITC on account of supplies made to SEZ Unit/SEZ Developer without payment of tax;

d. Refund of tax paid on supplies made to SEZ Unit/SEZ Developer with payment of tax;

e. Refund of unutilized ITC on account of accumulation due to inverted tax structure;

f. Refund to supplier of tax paid on deemed export supplies;

g. Refund to recipient of tax paid on deemed export supplies;

h. Refund of excess balance in the electronic cash ledger;

i. Refund of excess payment of tax;

j. Refund of tax paid on intra-State supply which is subsequently held to be inter-State supply and vice versa;

k. Refund on account of assessment/provisional assessment/appeal/any other order;

l. Refund on account of “any other” ground or reason.

Let’s take a look on highlights of new Circular :-

- GST RFD-01A will no longer in use for fresh applications w.e.f. 26/09/2019.

- List provided for documents to be uploaded along with application. (Four set of documents each of maximum 5 MB allowed to be uploaded)

- Neither the refund application in FORM GST RFD-01 nor any of the supporting documents shall be required to be physically submitted to the office of the jurisdictional proper officer.

- The application shall be deemed to have been filed on the date of generation of ARN and the time limit of 15 days to issue an acknowledgement or a deficiency memo, as the case may be, shall be counted from the said date.

- If a refund application is electronically transmitted to the wrong jurisdictional officer, he/she shall reassign it to the correct jurisdictional officer electronically.

- Deficiency memos shall not be issued in such cases merely on the ground that the applications were received electronically in the wrong jurisdiction.

- Any refund claim for a tax period may be filed only after furnishing all the returns in FORM GSTR-1 and FORM GSTR-3B which were due to be furnished on or before the date on which the refund application is being filed.

- Registered persons having aggregate turnover of up to Rs. 1.5 crore in the preceding financial year or the current financial year opting to file FORM GSTR-1 on quarterly basis, can only apply for refund on a quarterly basis or clubbing successive quarters.

- Once deficiency memo has been issued, the refund application would not be further processed and a fresh application would have to be filed. Any amount of input tax credit/cash debited from electronic credit/ cash ledger would be re-credited automatically once the deficiency memo has been issued.

- It is also clarified that since a refund application filed after correction of deficiency is treated as a fresh refund application, such a rectified refund application, submitted after correction of deficiencies, shall also have to be submitted within 2 years of the relevant date as required under section 54 of CGST Act 2017.

- Disbursement orders of refund of taxes under different heads will be issued by same authority who is processing the refund application. e.g. In case of Central Tax Authority, it would also disburse the refund of State/UT Tax, and in case of State Tax Authority, it will disburse CGST and IGST Tax refunds too.

-

The proper officer will be able to issue the payment order in FORM GST RFD-05 only after the selected bank account (i.e. mentioned in application of refund) has been validated.

Validation of Bank Accounts mentioned in Refund Application

The sanctioned refund amounts shall be disbursed through the Public Financial Management System (PFMS) of the Controller General of Accounts (CGA), Ministry of Finance, Government of India. On filing of a refund application in FORM GST RFD-01, the common portal shall generate a master file for the applicant containing the relevant details like name, GSTIN, bank account details etc. This master file shall be shared with PFMS for validation of the bank account details provided by the applicant in the refund application. Once the bank account is validated, PFMS will create a unique assessee code (combination of GSTIN + validated bank account number) for the applicant.

This unique assessee code will be used by PFMS for all refund payments made to the applicant in the said bank account. Therefore, in order to avoid repeat validations and generation of multiple unique assessee codes for the same GSTIN, it shall be advisable for the applicants to enter the same bank account details in successive refund applications submitted in FORM GST RFD-01.

In cases where an applicant wishes to avail the refund in a different bank account, which has not yet been validated, a new unique assessee code (comprising of GSTIN + new bank account) will be generated by PFMS after validation of the said bank account.

If the bank account details mentioned by an applicant in the refund application submitted in FORM GST RFD-01 are invalidated, an error message shall be transmitted by PFMS to the common portal electronically and the common portal shall make the error message available to the applicant and the refund officers on their dashboards.

On receiving such an error message, an applicant can:

a) rectify the invalidated bank account details by filing a non-core amendment in FORM GST REG-14; or

b) add a new bank account by filing a non-core amendment in FORM GST REG-14

The updated bank account details will be reflected in a drop-down menu on the dashboard. From this drop-down menu, the applicant can choose any bank account, including the ones rectified (option (a)) or newly added (option (b)), from the list of bank accounts available in his registration database.

The chosen bank account details will again be sent to PFMS for validation.

The proper officer will be able to issue the payment order in FORM GST RFD-05 only after the selected bank account has been validated.

Common Procedure to apply for all type of Refunds :-

- FORM GST RFD-01 shall be filled on the common portal by an applicant seeking refund under any category.

- Statements/declarations/undertakings shall be an integral part of Form GST RFD-01 itself. There is no need for separate attachment for such statements/declarations/undertakings.

- Documents, as required, to be uploaded along with application on portal.

- Once the application filed, an Application Reference Number (ARN) will be generated and amount would be debited from Electronic Cash/Credit ledger.

- As soon as the ARN is generated, the refund application along with all the supporting documents shall be transferred electronically to the jurisdictional proper officer who shall be able to view it on the system.

- The application shall be deemed to have been filed under sub-rule (2) of rule 90 of the CGST Rules on the date of generation of the said ARN and the time limit of 15 days to issue an acknowledgement or a deficiency memo, as the case may be, shall be counted from the said date.

- The acknowledgement for the complete application (FORM GST RFD-02) or deficiency memo (FORM GST RFD-03), as the case may be, would be issued electronically by the jurisdictional tax officer based on the documents so received from the common portal.

- After a deficiency memo has been issued, the refund application would not be further processed and a fresh application would have to be filed. Any amount of input tax credit/cash debited from electronic credit/ cash ledger would be re-credited automatically once the deficiency memo has been issued.

- It is further clarified that once an application has been submitted afresh, pursuant to a deficiency memo, the proper officer will not serve another deficiency memo with respect to the application for the same period, unless the deficiencies pointed out in the original deficiency memo remain un-rectified, either wholly or partly, or any other substantive deficiency is noticed subsequently.

Special Procedure for application for refund by Merchant Exporters:-

Rule 89(4B) of the CGST Rules provides that where the person claiming refund of unutilized input tax credit on account of zero-rated supplies without payment of tax has received supplies on which the supplier has availed the benefit of the Notification No. 40/2017 – Central Tax (Rate), dated 23rd October 2017 and notification No. 41/2017 – Integrated Tax (Rate) dated 23rd October 2017, the refund of input tax credit, availed in respect of such inputs received under the said notifications for export of goods, shall be granted.

This refund of accumulated ITC under rule 89(4B) of the CGST Rules shall be applied under the category “any other” instead of under the category “refund of unutilized ITC on account of exports without payment of tax” in FORM GST RFD-01 and shall be accompanied by all supporting documents required for substantiating the refund claim under the category “refund of unutilized ITC on account of exports without payment of tax”.

After scrutinizing the application for completeness and eligibility, if the proper officer is satisfied that the whole or any part of the amount claimed is payable as refund, he shall request the taxpayer, in writing, to debit the said amount from his electronic credit ledger through FORM GST DRC-03. Once the proof of such debit is received by the proper officer, he shall proceed to issue the refund order in FORM GST RFD-06 and the payment order in FORM GST RFD-05.

To know more about Merchant Export Transactions, refer GST on Merchant Export Transactions

Single Application for Multiple Tax Periods:-

The applicant, at his option, may file a refund claim for a tax period or by clubbing successive tax periods.

The period for which refund claim has been filed, however, cannot spread across different financial years.

Registered persons having aggregate turnover of up to Rs. 1.5 crore in the preceding financial year or the current financial year opting to file FORM GSTR-1 on quarterly basis, can only apply for refund on a quarterly basis or clubbing successive quarters as aforesaid.

In case of following category of refunds, application has to be filed chronologically for tax periods:-

- Refund of unutilized input tax credit (ITC) on account of exports without payment of tax;

- Refund of unutilized ITC on account of supplies made to SEZ Unit/SEZ Developer without payment of tax;

- Refund of unutilized ITC on account of accumulation due to inverted tax structure.

As per earlier advisory by GST Portal, in case refund application is not to be filed for any tax period, a declaration of `No Refund Application is to be provided.`{For eg:- April 2018 to June 2018 refund application cannot be filed till application or “No refund application declaration” is filed for any tax period prior to April 2018.}

After submitting a refund application under any of these categories for a certain period, shall not be subsequently allowed to file a refund claim under the same category for any previous period. This principle / limitation, however, shall not apply in cases where a fresh application is being filed pursuant to a deficiency memo having been issued earlier.

What if ‘application for refund’ transmitted to wrong Jurisdictional Officer :-

If a refund application is electronically transmitted to the wrong jurisdictional officer, he/she shall reassign it to the correct jurisdictional officer electronically as soon as possible, but not later than three working days, from the date of generation of the ARN.

Deficiency memos shall not be issued in such cases merely on the ground that the applications were received electronically in the wrong jurisdiction.

The facility to reassign such refund applications is already available with the Commissioner or the officer(s) authorized by him.

What if applicant is not assigned to any tax authority:-

The refund application in FORM GST RFD-01 filed by all taxpayers, who have already been assigned to the Centre or the State tax authorities, shall be automatically forwarded by the common portal to the concerned authority.

However, in case of unassigned taxpayers, The refund application in FORM GST RFD-01 shall be forwarded, for processing, by the common portal to the jurisdictional proper officer of the tax authority from which the taxpayer has originally migrated, in case he was migrated from earlier taxation system to GST.

As per circular, it seems that 100% of the taxpayers newly registered under GST regime are assigned to some tax authorities.

In case, during the processing of refunds, applicant is assigned to the counterpart tax authority, officers of authority to whom application forwarded by GST Portal, will continue to process these applications up to the stage of issuance of final order in FORM GST RFD-06 and the related payment order in FORM GST RFD-05.

However, if such an applicant gets assigned to one of the tax authorities after generation of the ARN and a deficiency memo gets issued for the refund application submitted by him, then the re-submitted refund application, after correction of deficiencies, shall be treated as a fresh refund application and shall be forwarded to the jurisdictional proper officer of the tax authority to which the taxpayer has now been assigned, irrespective of which authority handled the initial refund claim and issued the deficiency memo.

Guidelines in case of refunds of unutilized Input Tax Credit :-

There are three categories of tax refunds which are dependent on unutilized Input Tax Credit, viz. :-

- Refund of unutilized input tax credit (ITC) on account of exports without payment of tax;

- Refund of unutilized ITC on account of supplies made to SEZ Unit/SEZ Developer without payment of tax;

- Refund of unutilized ITC on account of accumulation due to inverted tax structure.

Followings are some additional guidelines in these category of refunds.

Uploading of GSTR-2A and Invoices

Applicants of refunds of unutilized ITC (under categories listed above), shall have to upload a copy of FORM GSTR-2A for the relevant period (or any prior or subsequent period(s) in which the relevant invoices have been auto-populated) for which the refund is claimed.

The proper officer shall rely upon FORM GSTR-2A as an evidence of the accountal of the supply by the corresponding supplier(s) in relation to which the input tax credit has been availed by the applicant.

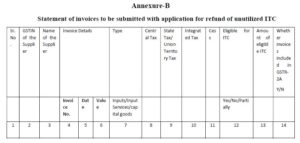

Such applicants shall also upload the details of all the invoices on the basis of which input tax credit has been availed during the relevant period for which the refund is being claimed, in the format enclosed as Annexure-B along with the application for refund claim.

Such availment of ITC will be subject to restriction imposed under sub-rule (4) in rule 36 of the CGST rules inserted vide Notification No. 49/2019-CT dated 09.10.2019. The applicant shall also declare the eligibility or otherwise of the input tax credit availed against the invoices related to the claim period in the said format for enabling the proper officer to determine the same.

Self-certified copies of invoices in relation to which the refund of ITC is being claimed and which are declared as eligible for ITC in Annexure – B, but which are not populated in FORM GSTR-2A, shall be uploaded by the applicant along with the application in FORM GST RFD 01.

It is emphasized that the proper officer shall not insist on the submission of an invoice (either original or duplicate) the details of which are available in FORM GSTR-2A of the relevant period uploaded by the applicant.

Order for Debit from Electronic Credit Ledger

In case of refunds (of untilized ITC) pertaining to categories listed above, the common portal calculates the refundable amount as the least of the following amounts:

a) The maximum refund amount as per the formula in rule 89(4) or rule 89(5) of the CGST Rules [formula is applied on the consolidated amount of ITC, i.e. Central tax + State tax/Union Territory tax +Integrated tax];

b) The balance in the electronic credit ledger of the applicant at the end of the tax period for which the refund claim is being filed after the return in FORM GSTR-3B for the said period has been filed; and

c) The balance in the electronic credit ledger of the applicant at the time of filing the refund application.

After calculating the least of the three amounts, as detailed above, the equivalent amount is to be debited from the electronic credit ledger of the applicant in the following order:

a) Integrated tax, to the extent of balance available;

b) Central tax and State tax/Union Territory tax, equally to the extent of balance available and in the event of a shortfall in the balance available in a particular electronic credit ledger (say, Central tax), the differential amount is to be debited from the other electronic credit ledger (i.e., State tax/Union Territory tax, in this case).

The order of debit described above, however, is not presently available on the common portal. Till the time such facility is made available on the common portal, the taxpayers are advised to follow the order as explained above for all refund applications.

However, for applications where this order is not adhered to by the applicant, no adverse view may be taken by the tax authorities.

The above system validations are being clarified so that there is no ambiguity in relation to the process through which an application in FORM GST RFD-01 is generated.

For all refund applications where refund of unutilized ITC of compensation cess is being claimed, the calculation of the refundable amount of compensation cess shall be done separately and the amount so calculated will be entirely debited from the balance of compensation cess available in the electronic credit ledger.

Documents required to be uploaded along with Application of Refund:-

Refund of unutilized ITC on account of exports without payment of tax

- Copy of GSTR-2A of the relevant period

- Statement of invoices (Annexure-B)

- Self-certified copies of invoices entered in Annexure-B whose details are not found in GSTR-2A of the relevant period

- BRC/FIRC in case of export of services and shipping bill (only in case of exports made through non-EDI ports) in case of goods

Refund of ITC unutilized on account of accumulation due to inverted tax structure

- Copy of GSTR-2A of the relevant period

- Statement of invoices (Annexure-B)

- Self-certified copies of invoices entered in Annexure-B whose details are not found in GSTR-2A of the relevant period

Refund of tax paid on export of services made with payment of tax

- BRC/FIRC /any other document indicating the receipt of sale proceeds of services

- Copy of GSTR-2A of the relevant period

- Statement of invoices (Annexure-B)

- Self-certified copies of invoices entered in Annexure-B whose details are not found in GSTR-2A of the relevant period

- Self-declaration regarding non-prosecution under sub-rule (1) of rule 91 of the CGST Rules for availing provisional refund

Refund of unutilized ITC on account of Supplies made to SEZ units/developer without payment of tax

- Copy of GSTR-2A of the relevant period

- Statement of invoices (Annexure-B)

- Self-certified copies of invoices entered in Annexure-B whose details are not found in GSTR-2A of the relevant period

- Endorsement(s) from the specified officer of the SEZ regarding receipt of goods/services for authorized operations under second proviso to rule 89(1)

Refund of tax paid on supplies made to SEZ units/developer with payment of tax :-

- Endorsement(s) from the specified officer of the SEZ regarding receipt of goods/services for authorized operations under second proviso to rule 89(1)

- Copy of GSTR-2A of the relevant period

- Self-certified copies of invoices entered in Annexure-B whose details are not found in GSTR-2A of the relevant period

- Self-declaration regarding non-prosecution under sub-rule (1) of rule 91 of the CGST Rules for availing provisional refund

Refund to supplier of tax paid on deemed export supplies

Documents required under Notification No. CGST-49/2017-Central Tax dated 18.10.2017 and Circular No. CIR-14/2017-GST dated 06.11.2017

Refund to recipient of tax paid on deemed export supplies

Documents required under Notification No. CGST-49/2017-Central Tax dated 18.10.2017 and Circular No. CIR-14/2017-GST dated 06.11.2017

Refund on account of assessment / provisional assessment / appeal / any other order

- Reference number of the order and a copy of the Assessment / Provisional Assessment / Appeal / Any Other Order

- Reference number/proof of payment of pre-deposit made earlier for which refund is being claimed

Refund on account of any other ground or reason

Documents in support of the claim

Special Instruction for officers to disburse refund in prescribed time:-

Section 56 of the CGST Act clearly states that if any tax ordered to be refunded is not refunded within 60 days of the date of receipt of application, interest at the rate of 6 per cent (notified vide notification No. 13/2017-Central Tax dated 28.06.2017) on the refund amount starting from the date immediately after the expiry of sixty days from the date of receipt of application (ARN) till the date of refund of such tax shall have to be paid to the applicant.

It may be noted that any tax shall be considered to have been refunded only when the amount has been credited to the bank account of the applicant. Therefore, interest will be calculated starting from the date immediately after the expiry of sixty days from the date of receipt of the application till the date on which the amount is credited to the bank account of the applicant.

Accordingly, all tax authorities are advised to issue the final sanction order in FORM GST RFD-06 and the payment order in FORM GST RFD-05 within 45 days of the date of generation of ARN, so that the disbursement is completed within 60 days.

[…] New Procedure for Refund-Fully Online Module-w.e.f. 26/09/2019 […]

[…] New Procedure for Refund-Fully Online Module-w.e.f. 26/09/2019 […]

I had filed my refund application, ” Refund due to inverted tax structure”, on 07-10-2019, through my portal. My bank account was validated on 13-10-2019, for which i got a mesagae on my registered mobile number & i could also see it on my portal.My assessing officer , DC-SGST issued RFD-02, RFD-6 & RFD-05, on 22-10-2019. The portal was showing that ” Disbursement request sent to PFMS”. On 16-11-2019, i received a message that my bank a/c has been rejected & again verify your bank a/c. So i again uploaded/verified the same bank a/c details on the portal , which was verified on 22-11-2019 and i could see it on my GST Portal.

But till today i.e 05-12-2019, the payment has not been credited in my bank a/c.

In between i created 3 tickets on GST compliance on different dates to register my complaint. But every time my complaint got AUTO resolved by stating that ” Contact your assessing officer & if he can’t resolve your problem then contact his senior officers.”

Please tell me how i can verify my PFMS status & how can i get my refudncredited in my a/c.

Refer Para 31 of CIR-125/44/2019-GST dated 18/11/2019.