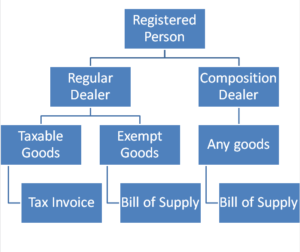

Returns System under GST for Regular Dealers (Other than Composition Dealers)

Under GST, every dealer registered as a Normal / Regular dealers have to file monthly returns of Outward Supplies and Inward Supplies. Outward Supplies means all sales of goods or services or both. Inward Supplies means all purchases…

Recent Comments